README

¶

README

¶

CREX

CREX 是一个用Golang语言开发的量化交易库。支持tick级别数字币期货平台的回测和实盘。实盘与回测无缝切换,无需更改代码。

回测

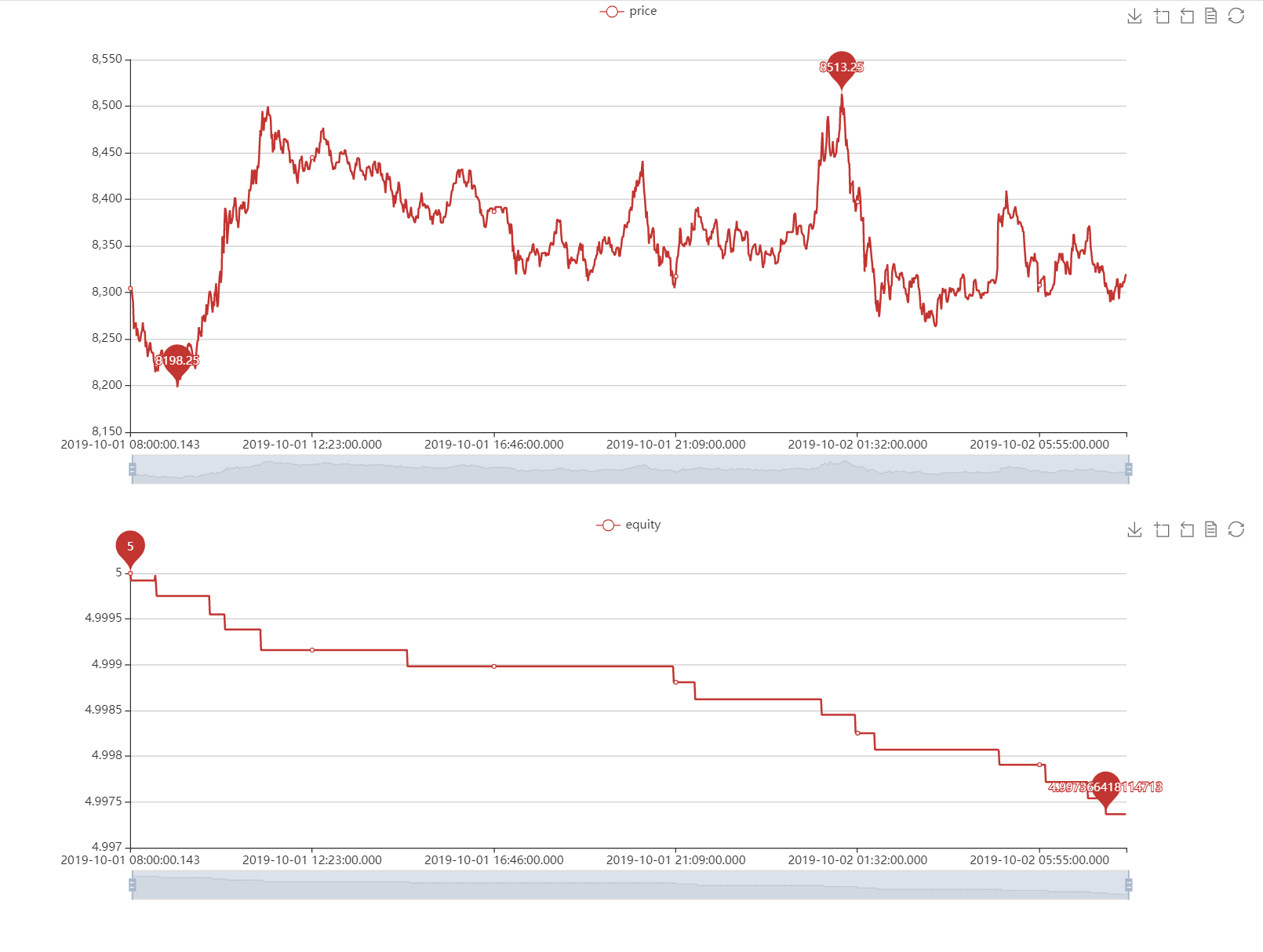

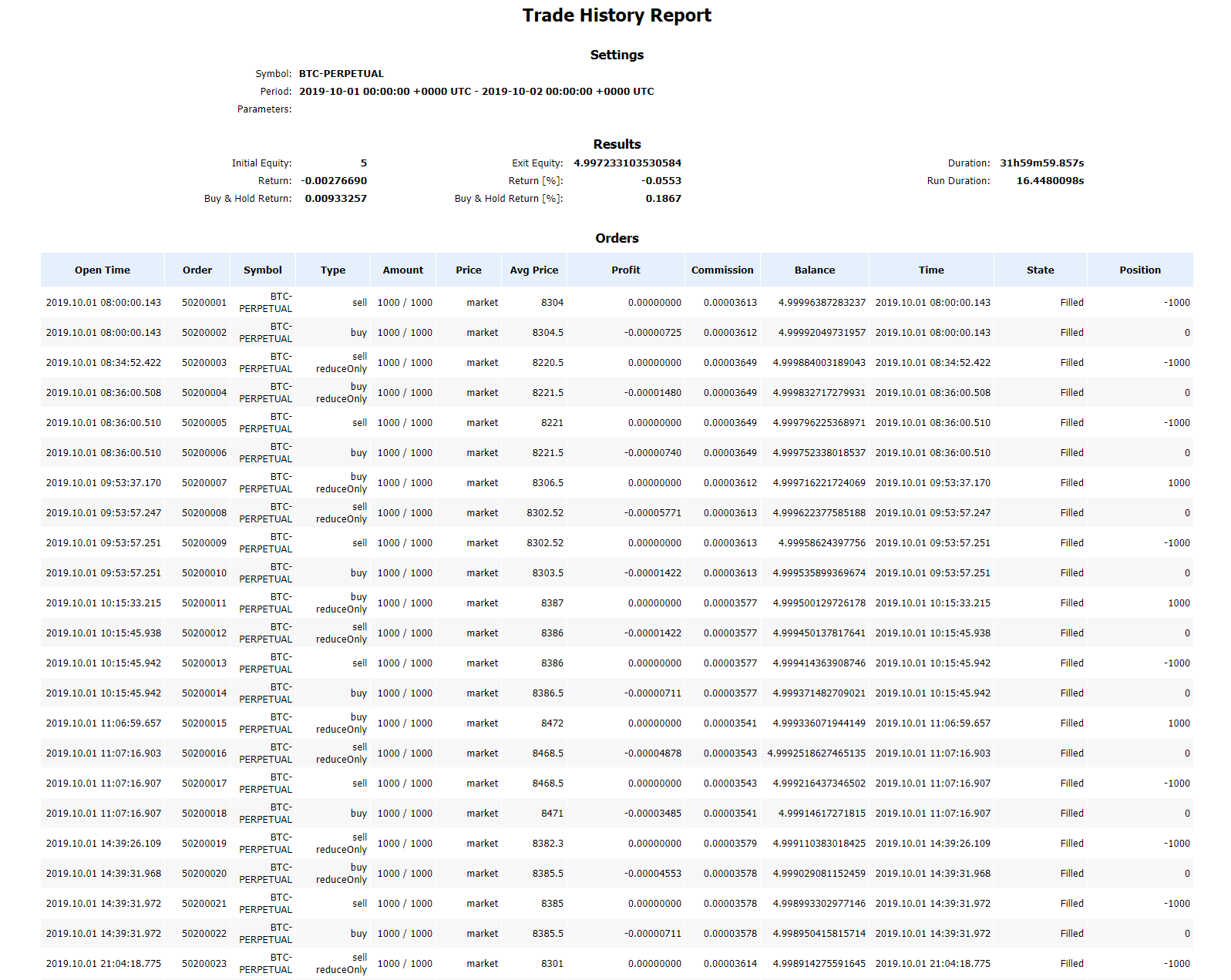

示例 @backtest

交易结果

开源策略

https://github.com/coinrust/trading-strategies

主要特性

- 使用简单

- Tick级别回测

- 实盘、回测公用策略代码

- 支持 WebSocket 共有和私有订阅

- 支持期货、现货回测

- 支持期货双向合约,正反向合约

支持交易所

CREX库当前支持以下8个加密货币交易市场和交易API

| logo | id | name | ver | ws | doc |

|---|---|---|---|---|---|

|

binancefutures | Binance Futures | 1 | N | API |

|

bitmex | BitMEX | 1 | Y | API |

|

deribit | Deribit | 2 | Y | API |

|

bybit | Bybit | 2 | Y | API |

|

hbdm | Huobi DM | 1 | Y | API |

|

hbdmswap | Huobi Swap | 1 | Y | API |

|

okexfutures | OKEX Futures | 3 | Y | API |

|

okexswap | OKEX Swap | 3 | Y | API |

示例

package main

import (

. "github.com/evzpav/crex"

"github.com/evzpav/crex/exchanges"

"log"

"time"

)

type BasicStrategy struct {

StrategyBase

}

func (s *BasicStrategy) OnInit() error {

return nil

}

func (s *BasicStrategy) OnTick() error {

currency := "BTC"

symbol := "BTC-PERPETUAL"

balance, err := s.Exchange.GetBalance(currency)

if err != nil {

log.Fatal(err)

}

log.Printf("balance: %#v", balance)

s.Exchange.GetOrderBook(symbol, 10)

s.Exchange.OpenLong(symbol, OrderTypeLimit, 5000, 10)

s.Exchange.CloseLong(symbol, OrderTypeLimit, 6000, 10)

//Trailing Stop Market Order - sell stop loss order for long position

callbackRate := 5.0 // from 0.1% until 5% allowed

s.Exchange.PlaceOrder(symbol, Sell, OrderTypeTrailingStopMarket, 0.0, 10,

OrderCallbackRateOption(callbackRate), OrderReduceOnlyOption(true))

s.Exchange.PlaceOrder(symbol,

Buy, OrderTypeLimit, 1000.0, 10, OrderPostOnlyOption(true))

s.Exchange.GetOpenOrders(symbol)

s.Exchange.GetPositions(symbol)

return nil

}

func (s *BasicStrategy) Run() error {

// run loop

for {

s.OnTick()

time.Sleep(1 * time.Second)

}

return nil

}

func (s *BasicStrategy) OnExit() error {

return nil

}

func main() {

exchange := exchanges.NewExchange(exchanges.Deribit,

ApiProxyURLOption("socks5://127.0.0.1:1080"), // 使用代理

//ApiAccessKeyOption("[accessKey]"),

//ApiSecretKeyOption("[secretKey]"),

ApiTestnetOption(true))

s := &BasicStrategy{}

s.Setup(TradeModeLiveTrading, exchange)

s.OnInit()

s.Run()

s.OnExit()

}

WebSocket 示例

package main

import (

. "github.com/evzpav/crex"

"github.com/evzpav/crex/exchanges"

"log"

)

func main() {

ws := exchanges.NewExchange(exchanges.OkexFutures,

ApiProxyURLOption("socks5://127.0.0.1:1080"), // 使用代理

//ApiAccessKeyOption("[accessKey]"),

//ApiSecretKeyOption("[secretKey]"),

//ApiPassPhraseOption("[passphrase]"),

ApiWebSocketOption(true)) // 开启 WebSocket

market := Market{

Symbol: "BTC-USD-200626",

}

// 订阅订单薄

ws.SubscribeLevel2Snapshots(market, func(ob *OrderBook) {

log.Printf("%#v", ob)

})

// 订阅成交记录

ws.SubscribeTrades(market, func(trades []*Trade) {

log.Printf("%#v", trades)

})

// 订阅订单成交信息

ws.SubscribeOrders(market, func(orders []*Order) {

log.Printf("%#v", orders)

})

// 订阅持仓信息

ws.SubscribePositions(market, func(positions []*Position) {

log.Printf("%#v", positions)

})

select {}

}

回测数据

1. 标准 CSV 数据格式

- 列定界符: , (逗号)

- 换行标记: \n (LF)

- 日期时间格式: Unix 时间戳 (ms)

时间格式

| 列名 | 描述 |

|---|---|

| t | Unix 时间戳 (ms) |

| asks[0-X].price | 卖单价(升序) |

| asks[0-X].amount | 卖单量 |

| bids[0-X].price | 买单价(降序) |

| bids[0-X].amount | 买单量 |

样本数据示例

t,asks[0].price,asks[0].amount,asks[1].price,asks[1].amount,asks[2].price,asks[2].amount,asks[3].price,asks[3].amount,asks[4].price,asks[4].amount,asks[5].price,asks[5].amount,asks[6].price,asks[6].amount,asks[7].price,asks[7].amount,asks[8].price,asks[8].amount,asks[9].price,asks[9].amount,bids[0].price,bids[0].amount,bids[1].price,bids[1].amount,bids[2].price,bids[2].amount,bids[3].price,bids[3].amount,bids[4].price,bids[4].amount,bids[5].price,bids[5].amount,bids[6].price,bids[6].amount,bids[7].price,bids[7].amount,bids[8].price,bids[8].amount,bids[9].price,bids[9].amount

1569888000143,8304.5,7010,8305,60,8305.5,1220,8306,80,8307,200,8307.5,1650,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,90,8300,71320,8299.5,310

1569888000285,8304.5,7010,8305,60,8305.5,1220,8306,80,8307,200,8307.5,1650,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

1569888000307,8304.5,7010,8305,60,8305.5,1220,8306,80,8307,200,8307.5,11010,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

1569888000309,8304.5,7010,8305,60,8305.5,1220,8306,80,8307,200,8307.5,20370,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

1569888000406,8304.5,7010,8305,60,8305.5,1220,8306,80,8307,8960,8307.5,11010,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

1569888000500,8304.5,7010,8305,60,8305.5,1220,8306,80,8307,200,8307.5,20370,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

1569888000522,8304.5,10270,8305,60,8305.5,1220,8306,80,8307,200,8307.5,20370,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185750,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

1569888000527,8304.5,10270,8305,60,8305.5,1220,8306,80,8307,200,8307.5,20370,8308,68260,8308.5,120000,8309,38400,8309.5,8400,8304,185010,8303.5,52200,8303,20600,8302.5,4500,8302,2000,8301.5,18200,8301,18000,8300.5,5090,8300,71320,8299.5,310

2. MongoDB (推荐)

- Database. for example: tick_db

- Collection. for example: deribit:BTC-PERPETUAL

- Document: t: timestamp (ms) a: asks Array [[ask_price_0,ask_amount_0],[ask_price_1,ask_amount_1],...] b: bids Array [[bid_price_0,ask_amount_0],[bid_price_1,bid_amount_1],...]

{"_id":{"$oid":"5eb946d88316c7a9c541705c"},"t":{"$numberLong":"1569888000143"},"a":[[8304.5,7010],[8305,60],[8305.5,1220],[8306,80],[8307,200],[8307.5,1650],[8308,68260],[8308.5,120000],[8309,38400],[8309.5,8400]],"b":[[8304,185750],[8303.5,52200],[8303,20600],[8302.5,4500],[8302,2000],[8301.5,18200],[8301,18000],[8300.5,90],[8300,71320],[8299.5,310]]}

数据处理示例

Example of importing data into a database:

cd ./cmd/deribit-data-to-db

go build

./deribit-data-to-db

TODO

- Paper trading.

QQ群

QQ群: 932289088

捐赠

| METHOD | ADDRESS |

|---|---|

| BTC | 1Nk4AsGj5HEJ5csRenTUPab1sjUySCZ3Pq |

| ETH | 0xa74eade7ea08a8c48d7de4d582fac145afc86e3d |

LICENSE

MIT ©coinrust

Documentation

¶

Documentation

¶

Index ¶

- Constants

- Variables

- func GenOrderId() string

- func SetIdGenerate(g *utils.IdGenerate)

- type ApiOption

- func ApiAccessKeyOption(accessKey string) ApiOption

- func ApiApiURLOption(apiURL string) ApiOption

- func ApiDebugModeOption(debugMode bool) ApiOption

- func ApiHttpClientOption(httpClient *http.Client) ApiOption

- func ApiPassPhraseOption(passPhrase string) ApiOption

- func ApiProxyURLOption(proxyURL string) ApiOption

- func ApiSecretKeyOption(secretKey string) ApiOption

- func ApiTestnetOption(testnet bool) ApiOption

- func ApiWebSocketOption(enabled bool) ApiOption

- func ApiWsURLOption(wsURL string) ApiOption

- type Balance

- type CStrategyBase

- func (s *CStrategyBase) GetOptions() (optionMap map[string]*StrategyOption)

- func (s *CStrategyBase) IsStopped() bool

- func (s *CStrategyBase) Name() string

- func (s *CStrategyBase) SetName(name string)

- func (s *CStrategyBase) SetOptions(options map[string]interface{}) error

- func (s *CStrategyBase) SetSelf(self Strategy) error

- func (s *CStrategyBase) Setup(mode TradeMode, exchanges ...interface{}) error

- func (s *CStrategyBase) StopNow()

- func (s *CStrategyBase) TradeMode() TradeMode

- type Direction

- type EmptyExchangeLogger

- func (l *EmptyExchangeLogger) Debug(args ...interface{})

- func (l *EmptyExchangeLogger) Debugf(template string, args ...interface{})

- func (l *EmptyExchangeLogger) Debugw(msg string, keysAndValues ...interface{})

- func (l *EmptyExchangeLogger) Error(args ...interface{})

- func (l *EmptyExchangeLogger) Errorf(template string, args ...interface{})

- func (l *EmptyExchangeLogger) Errorw(msg string, keysAndValues ...interface{})

- func (l *EmptyExchangeLogger) Info(args ...interface{})

- func (l *EmptyExchangeLogger) Infof(template string, args ...interface{})

- func (l *EmptyExchangeLogger) Infow(msg string, keysAndValues ...interface{})

- func (l *EmptyExchangeLogger) Sync()

- func (l *EmptyExchangeLogger) Warn(args ...interface{})

- func (l *EmptyExchangeLogger) Warnf(template string, args ...interface{})

- func (l *EmptyExchangeLogger) Warnw(msg string, keysAndValues ...interface{})

- type Event

- type Exchange

- type ExchangeLogger

- type ExchangeSim

- type IBacktest

- type Item

- type LogItem

- type LogItems

- type LogStats

- type Market

- type Order

- type OrderBook

- func (o *OrderBook) Ask() (result Item)

- func (o *OrderBook) AskAvePrice(size float64) float64

- func (o *OrderBook) AskPrice() (result float64)

- func (o *OrderBook) Bid() (result Item)

- func (o *OrderBook) BidAvePrice(size float64) float64

- func (o *OrderBook) BidPrice() (result float64)

- func (o *OrderBook) MatchAsks(size float64) (filledSize float64, avgPrice float64)

- func (o *OrderBook) MatchBids(size float64) (filledSize float64, avgPrice float64)

- func (o *OrderBook) MatchOrderbook(size float64, ob []Item) (filledSize float64, avgPrice float64)

- func (o *OrderBook) Price() float64

- func (o *OrderBook) Table() string

- type OrderOption

- type OrderParameter

- type OrderStatus

- type OrderType

- type Parameters

- type PlaceOrderOption

- func OrderActivationPriceOption(activationPrice float64) PlaceOrderOption

- func OrderBasePriceOption(basePrice float64) PlaceOrderOption

- func OrderCallbackRateOption(callbackRate float64) PlaceOrderOption

- func OrderClientOIdOption(clientOId string) PlaceOrderOption

- func OrderClosePositionOption(closePosition bool) PlaceOrderOption

- func OrderPostOnlyOption(postOnly bool) PlaceOrderOption

- func OrderPriceTypeOption(priceType string) PlaceOrderOption

- func OrderReduceOnlyOption(reduceOnly bool) PlaceOrderOption

- func OrderStopPxOption(stopPx float64) PlaceOrderOption

- func OrderTimeInForceOption(timeInForce string) PlaceOrderOption

- type PlaceOrderParameter

- type Position

- type Record

- type SpotAsset

- type SpotBalance

- type SpotExchange

- type SpotExchangeSim

- type SpotStrategyBase

- func (s *SpotStrategyBase) GetOptions() (optionMap map[string]*StrategyOption)

- func (s *SpotStrategyBase) Name() string

- func (s *SpotStrategyBase) SetName(name string)

- func (s *SpotStrategyBase) SetOptions(options map[string]interface{}) error

- func (s *SpotStrategyBase) SetSelf(self Strategy) error

- func (s *SpotStrategyBase) Setup(mode TradeMode, exchanges ...interface{}) error

- func (s *SpotStrategyBase) TradeMode() TradeMode

- type Stats

- type Strategy

- type StrategyBase

- func (s *StrategyBase) GetOptions() (optionMap map[string]*StrategyOption)

- func (s *StrategyBase) IsStopped() bool

- func (s *StrategyBase) Name() string

- func (s *StrategyBase) SetName(name string)

- func (s *StrategyBase) SetOptions(options map[string]interface{}) error

- func (s *StrategyBase) SetSelf(self Strategy) error

- func (s *StrategyBase) Setup(mode TradeMode, exchanges ...interface{}) error

- func (s *StrategyBase) StopNow()

- func (s *StrategyBase) TradeMode() TradeMode

- type StrategyOption

- type Trade

- type TradeMode

- type WSEvent

- type WebSocket

Constants ¶

const ( SimEventKey = "event" SimEventOrder = "order" // 委托 SimEventDeal = "deal" // 成交 )

回测交易撮合事件类型

const ( ContractTypeNone = "" // Non-delivery contract 非交割合约 ContractTypeW1 = "W1" // week 当周合约 ContractTypeW2 = "W2" // two week 次周合约 ContractTypeM1 = "M1" // month 月合约 ContractTypeQ1 = "Q1" // quarter 季度合约 ContractTypeQ2 = "Q2" // two quarter 次季度合约 )

ContractType 合约类型

const ( PERIOD_1MIN = "1m" PERIOD_3MIN = "3m" PERIOD_5MIN = "5m" PERIOD_15MIN = "15m" PERIOD_30MIN = "30m" PERIOD_60MIN = "60m" PERIOD_1H = "1h" PERIOD_2H = "2h" PERIOD_3H = "3h" PERIOD_4H = "4h" PERIOD_6H = "6h" PERIOD_8H = "8h" PERIOD_12H = "12h" PERIOD_1DAY = "1d" PERIOD_3DAY = "3d" PERIOD_1WEEK = "1w" PERIOD_1MONTH = "1M" PERIOD_1YEAR = "1y" )

K线周期

const (

// StrategyOptionTag 选项Tag

StrategyOptionTag = "opt"

)

Variables ¶

Functions ¶

func GenOrderId ¶

func GenOrderId() string

func SetIdGenerate ¶

func SetIdGenerate(g *utils.IdGenerate)

Types ¶

type ApiOption ¶

type ApiOption func(p *Parameters)

func ApiAccessKeyOption ¶

func ApiApiURLOption ¶

func ApiDebugModeOption ¶

func ApiHttpClientOption ¶

func ApiPassPhraseOption ¶

func ApiProxyURLOption ¶

func ApiSecretKeyOption ¶

func ApiTestnetOption ¶

func ApiWebSocketOption ¶

func ApiWsURLOption ¶

type CStrategyBase ¶

type CStrategyBase struct {

Exchanges []Exchange

SpotExchanges []SpotExchange

// contains filtered or unexported fields

}

组合策略,期现等 CStrategyBase Strategy base class

func (*CStrategyBase) GetOptions ¶

func (s *CStrategyBase) GetOptions() (optionMap map[string]*StrategyOption)

GetOptions Returns the options of strategy

func (*CStrategyBase) IsStopped ¶

func (s *CStrategyBase) IsStopped() bool

func (*CStrategyBase) Name ¶

func (s *CStrategyBase) Name() string

func (*CStrategyBase) SetName ¶

func (s *CStrategyBase) SetName(name string)

func (*CStrategyBase) SetOptions ¶

func (s *CStrategyBase) SetOptions(options map[string]interface{}) error

SetOptions Sets the options for the strategy

func (*CStrategyBase) SetSelf ¶

func (s *CStrategyBase) SetSelf(self Strategy) error

SetSelf 设置 self 对象

func (*CStrategyBase) Setup ¶

func (s *CStrategyBase) Setup(mode TradeMode, exchanges ...interface{}) error

Setup Setups the exchanges

func (*CStrategyBase) StopNow ¶

func (s *CStrategyBase) StopNow()

func (*CStrategyBase) TradeMode ¶

func (s *CStrategyBase) TradeMode() TradeMode

type EmptyExchangeLogger ¶

type EmptyExchangeLogger struct {

}

EmptyExchangeLogger 交易所撮合日志

func (*EmptyExchangeLogger) Debug ¶

func (l *EmptyExchangeLogger) Debug(args ...interface{})

func (*EmptyExchangeLogger) Debugf ¶

func (l *EmptyExchangeLogger) Debugf(template string, args ...interface{})

func (*EmptyExchangeLogger) Debugw ¶

func (l *EmptyExchangeLogger) Debugw(msg string, keysAndValues ...interface{})

func (*EmptyExchangeLogger) Error ¶

func (l *EmptyExchangeLogger) Error(args ...interface{})

func (*EmptyExchangeLogger) Errorf ¶

func (l *EmptyExchangeLogger) Errorf(template string, args ...interface{})

func (*EmptyExchangeLogger) Errorw ¶

func (l *EmptyExchangeLogger) Errorw(msg string, keysAndValues ...interface{})

func (*EmptyExchangeLogger) Info ¶

func (l *EmptyExchangeLogger) Info(args ...interface{})

func (*EmptyExchangeLogger) Infof ¶

func (l *EmptyExchangeLogger) Infof(template string, args ...interface{})

func (*EmptyExchangeLogger) Infow ¶

func (l *EmptyExchangeLogger) Infow(msg string, keysAndValues ...interface{})

func (*EmptyExchangeLogger) Sync ¶

func (l *EmptyExchangeLogger) Sync()

func (*EmptyExchangeLogger) Warn ¶

func (l *EmptyExchangeLogger) Warn(args ...interface{})

func (*EmptyExchangeLogger) Warnf ¶

func (l *EmptyExchangeLogger) Warnf(template string, args ...interface{})

func (*EmptyExchangeLogger) Warnw ¶

func (l *EmptyExchangeLogger) Warnw(msg string, keysAndValues ...interface{})

type Event ¶

type Event struct {

// contains filtered or unexported fields

}

type Exchange ¶

type Exchange interface {

// 获取 Exchange 名称

GetName() (name string)

// 获取交易所时间(ms)

GetTime() (tm int64, err error)

// 获取账号余额

GetBalance(currency string) (result *Balance, err error)

// 获取订单薄(OrderBook)

GetOrderBook(symbol string, depth int) (result *OrderBook, err error)

// 获取K线数据

// period: 数据周期. 分钟或者关键字1m(minute) 1h 1d 1w 1M(month) 1y 枚举值:1 3 5 15 30 60 120 240 360 720 "5m" "4h" "1d" ...

GetRecords(symbol string, period string, from int64, end int64, limit int) (records []*Record, err error)

// 设置合约类型

// currencyPair: 交易对,如: BTC-USD(OKEX) BTC(HBDM)

// contractType: W1,W2,Q1,Q2

SetContractType(currencyPair string, contractType string) (err error)

// 获取当前设置的合约ID

GetContractID() (symbol string, err error)

// 设置杠杆大小

SetLeverRate(value float64) (err error)

// 开多

OpenLong(symbol string, orderType OrderType, price float64, size float64) (result *Order, err error)

// 开空

OpenShort(symbol string, orderType OrderType, price float64, size float64) (result *Order, err error)

// 平多

CloseLong(symbol string, orderType OrderType, price float64, size float64) (result *Order, err error)

// 平空

CloseShort(symbol string, orderType OrderType, price float64, size float64) (result *Order, err error)

// 下单

PlaceOrder(symbol string, direction Direction, orderType OrderType, price float64, size float64,

opts ...PlaceOrderOption) (result *Order, err error)

// 获取活跃委托单列表

GetOpenOrders(symbol string, opts ...OrderOption) (result []*Order, err error)

// 获取委托信息

GetOrder(symbol string, id string, opts ...OrderOption) (result *Order, err error)

// 撤销全部委托单

CancelAllOrders(symbol string, opts ...OrderOption) (err error)

// 撤销单个委托单

CancelOrder(symbol string, id string, opts ...OrderOption) (result *Order, err error)

// 修改委托

AmendOrder(symbol string, id string, price float64, size float64, opts ...OrderOption) (result *Order, err error)

// 获取持仓

GetPositions(symbol string) (result []*Position, err error)

// 订阅成交记录

SubscribeTrades(market Market, callback func(trades []*Trade)) error

// 订阅L2 OrderBook

SubscribeLevel2Snapshots(market Market, callback func(ob *OrderBook)) error

// 订阅委托

SubscribeOrders(market Market, callback func(orders []*Order)) error

// 订阅持仓

SubscribePositions(market Market, callback func(positions []*Position)) error

// 调用其他功能

IO(name string, params string) (string, error)

}

Exchange 交易所接口

type ExchangeLogger ¶

type ExchangeLogger interface {

// Debug Using:log.Debug("test")

Debug(args ...interface{})

// Debugf Using:log.Debugf("test:%s", err)

Debugf(template string, args ...interface{})

// Debugw Using:log.Debugw("test", "field1", "value1", "field2", "value2")

Debugw(msg string, keysAndValues ...interface{})

Info(args ...interface{})

Infof(template string, args ...interface{})

Infow(msg string, keysAndValues ...interface{})

Warn(args ...interface{})

Warnf(template string, args ...interface{})

Warnw(msg string, keysAndValues ...interface{})

Error(args ...interface{})

Errorf(template string, args ...interface{})

Errorw(msg string, keysAndValues ...interface{})

// 同步,确保日志写入

Sync()

}

ExchangeLogger 交易所撮合日志

type ExchangeSim ¶

type ExchangeSim interface {

// 设置回测组件

SetBacktest(backtest IBacktest)

// 设置交易撮合日志组件

SetExchangeLogger(l ExchangeLogger)

// 运行一次(回测系统调用)

RunEventLoopOnce() (err error) // Run sim match for backtest only

}

ExchangeSim 模拟交易所接口

type LogItem ¶

type LogItem struct {

Time time.Time `json:"time"`

RawTime time.Time `json:"raw_time"`

Prices []float64 `json:"prices"`

//Ask float64 `json:"ask"`

//Bid float64 `json:"bid"`

Stats []LogStats `json:"stats"`

}

func (*LogItem) TotalEquity ¶

type Order ¶

type Order struct {

ID string `json:"id"` // ID

ClientOId string `json:"client_oid"` // 客户端订单ID

Symbol string `json:"symbol"` // 标

Time time.Time `json:"time"` // 订单时间

Price float64 `json:"price"` // 价格

StopPx float64 `json:"stop_px"` // 触发价

Amount float64 `json:"amount"` // 委托数量

AvgPrice float64 `json:"avg_price"` // 平均成交价

FilledAmount float64 `json:"filled_amount"` // 成交数量

Direction Direction `json:"direction"` // 委托方向

Type OrderType `json:"type"` // 委托类型

PostOnly bool `json:"post_only"` // 只做Maker选项

ReduceOnly bool `json:"reduce_only"` // 只减仓选项

Commission float64 `json:"commission"` // 支付的佣金

Pnl float64 `json:"pnl"` // 盈亏

UpdateTime time.Time `json:"update_time"` // 更新时间

Status OrderStatus `json:"status"` // 委托状态

ActivatePrice string `json:"activatePrice"`

PriceRate string `json:"priceRate"`

ClosePosition bool `json:"closePosition"`

}

Order 委托

type OrderBook ¶

func (*OrderBook) AskAvePrice ¶

func (*OrderBook) BidAvePrice ¶

func (*OrderBook) MatchOrderbook ¶

type OrderParameter ¶

type OrderParameter struct {

Stop bool // 是否是触发委托

}

func ParseOrderParameter ¶

func ParseOrderParameter(opts ...OrderOption) *OrderParameter

type OrderStatus ¶

type OrderStatus int

OrderStatus 委托状态

const ( OrderStatusCreated OrderStatus = iota // 创建委托 OrderStatusRejected // 委托被拒绝 OrderStatusNew // 委托待成交 OrderStatusPartiallyFilled // 委托部分成交 OrderStatusFilled // 委托完全成交 OrderStatusCancelPending // 委托取消 OrderStatusCancelled // 委托被取消 OrderStatusUntriggered // 等待触发条件委托单 OrderStatusTriggered // 已触发条件单 )

func (OrderStatus) String ¶

func (s OrderStatus) String() string

type Parameters ¶

type PlaceOrderOption ¶

type PlaceOrderOption func(p *PlaceOrderParameter)

订单选项

func OrderActivationPriceOption ¶

func OrderActivationPriceOption(activationPrice float64) PlaceOrderOption

func OrderBasePriceOption ¶

func OrderBasePriceOption(basePrice float64) PlaceOrderOption

基础价格选项(如: bybit 需要提供此参数)

func OrderCallbackRateOption ¶

func OrderCallbackRateOption(callbackRate float64) PlaceOrderOption

func OrderClientOIdOption ¶

func OrderClientOIdOption(clientOId string) PlaceOrderOption

func OrderClosePositionOption ¶

func OrderClosePositionOption(closePosition bool) PlaceOrderOption

func OrderPriceTypeOption ¶

func OrderPriceTypeOption(priceType string) PlaceOrderOption

OrderPriceType 选项

func OrderTimeInForceOption ¶

func OrderTimeInForceOption(timeInForce string) PlaceOrderOption

type PlaceOrderParameter ¶

type PlaceOrderParameter struct {

BasePrice float64

StopPx float64

PostOnly bool

ReduceOnly bool

PriceType string

ClientOId string

TimeInForce string

ActivationPrice float64

CallbackRate float64

ClosePosition bool

}

func ParsePlaceOrderParameter ¶

func ParsePlaceOrderParameter(opts ...PlaceOrderOption) *PlaceOrderParameter

type Position ¶

type Position struct {

Symbol string `json:"symbol"` // 标

OpenTime time.Time `json:"open_time"` // 开仓时间

OpenPrice float64 `json:"open_price"` // 开仓价

Size float64 `json:"size"` // 仓位大小

AvgPrice float64 `json:"avg_price"` // 平均价

Profit float64 `json:"profit"` //浮动盈亏

MarginType string `json:"marginType"`

IsAutoAddMargin bool `json:"isAutoAddMargin"`

IsolatedMargin float64 `json:"isolatedMargin"`

Leverage float64 `json:"leverage"`

LiquidationPrice float64 `json:"liquidationPrice"`

MarkPrice float64 `json:"markPrice"`

MaxNotionalValue float64 `json:"maxNotionalValue"`

PositionSide string `json:"positionSide"`

}

Position 持仓

type Record ¶

type Record struct {

Symbol string `json:"symbol"` // 标

Timestamp time.Time `json:"timestamp"` // 时间

Open float64 `json:"open"` // 开盘价

High float64 `json:"high"` // 最高价

Low float64 `json:"low"` // 最低价

Close float64 `json:"close"` // 收盘价

Volume float64 `json:"volume"` // 量

}

Record 表示K线数据

type SpotAsset ¶

type SpotAsset struct {

Name string // BTC

Available float64 // 可用

Frozen float64 // 冻结

Borrow float64 // 借币

}

现货资产

type SpotBalance ¶

SpotBalance 现货账号资产

type SpotExchange ¶

type SpotExchange interface {

// 获取 Exchange 名称

GetName() (name string)

// 获取交易所时间(ms)

GetTime() (tm int64, err error)

// 获取账号余额

GetBalance(currency string) (result *SpotBalance, err error)

// 获取订单薄(OrderBook)

GetOrderBook(symbol string, depth int) (result *OrderBook, err error)

// 获取K线数据

// period: 数据周期. 分钟或者关键字1m(minute) 1h 1d 1w 1M(month) 1y 枚举值:1 3 5 15 30 60 120 240 360 720 "5m" "4h" "1d" ...

GetRecords(symbol string, period string, from int64, end int64, limit int) (records []*Record, err error)

// 买

Buy(symbol string, orderType OrderType, price float64, size float64) (result *Order, err error)

// 卖

Sell(symbol string, orderType OrderType, price float64, size float64) (result *Order, err error)

// 下单

PlaceOrder(symbol string, direction Direction, orderType OrderType, price float64, size float64,

opts ...PlaceOrderOption) (result *Order, err error)

// 获取活跃委托单列表

GetOpenOrders(symbol string, opts ...OrderOption) (result []*Order, err error)

// 获取历史委托列表

GetHistoryOrders(symbol string, opts ...OrderOption) (result []*Order, err error)

// 获取委托信息

GetOrder(symbol string, id string, opts ...OrderOption) (result *Order, err error)

// 撤销全部委托单

CancelAllOrders(symbol string, opts ...OrderOption) (err error)

// 撤销单个委托单

CancelOrder(symbol string, id string, opts ...OrderOption) (result *Order, err error)

// 调用其他功能

IO(name string, params string) (string, error)

}

SpotExchange 现货交易所接口

type SpotExchangeSim ¶

type SpotExchangeSim interface {

SpotExchange

// 设置交易撮合日志组件

SetExchangeLogger(l ExchangeLogger)

// 运行一次(回测系统调用)

RunEventLoopOnce() (err error) // Run sim match for backtest only

}

SpotExchangeSim 模拟交易所接口

type SpotStrategyBase ¶

type SpotStrategyBase struct {

Exchanges []SpotExchange

Exchange SpotExchange

// contains filtered or unexported fields

}

SpotStrategyBase Strategy base class

func (*SpotStrategyBase) GetOptions ¶

func (s *SpotStrategyBase) GetOptions() (optionMap map[string]*StrategyOption)

GetOptions Returns the options of strategy

func (*SpotStrategyBase) Name ¶

func (s *SpotStrategyBase) Name() string

func (*SpotStrategyBase) SetName ¶

func (s *SpotStrategyBase) SetName(name string)

func (*SpotStrategyBase) SetOptions ¶

func (s *SpotStrategyBase) SetOptions(options map[string]interface{}) error

SetOptions Sets the options for the strategy

func (*SpotStrategyBase) SetSelf ¶

func (s *SpotStrategyBase) SetSelf(self Strategy) error

SetSelf 设置 self 对象

func (*SpotStrategyBase) Setup ¶

func (s *SpotStrategyBase) Setup(mode TradeMode, exchanges ...interface{}) error

Setup Setups the exchanges

func (*SpotStrategyBase) TradeMode ¶

func (s *SpotStrategyBase) TradeMode() TradeMode

type Stats ¶

type Stats struct {

Start time.Time `json:"start"`

End time.Time `json:"end"`

Duration time.Duration `json:"duration"`

RunDuration time.Duration `json:"run_duration"`

EntryPrice float64 `json:"entry_price"`

ExitPrice float64 `json:"exit_price"`

EntryEquity float64 `json:"entry_equity"`

ExitEquity float64 `json:"exit_equity"`

BaHReturn float64 `json:"bah_return"` // Buy & Hold Return

BaHReturnPnt float64 `json:"bah_return_pnt"` // Buy & Hold Return

EquityReturn float64 `json:"equity_return"`

EquityReturnPnt float64 `json:"equity_return_pnt"`

AnnReturn float64 `json:"ann_return"` // 年化收益率

MaxDrawDown float64 `json:"max_draw_down"` // 最大回撤

}

Stats Back testing Statistics

func (*Stats) PrintResult ¶

func (s *Stats) PrintResult()

type Strategy ¶

type Strategy interface {

Name() string

SetName(name string)

SetSelf(self Strategy) error

//Setup(mode TradeMode, exchanges ...Exchange) error

Setup(mode TradeMode, exchanges ...interface{}) error

IsStopped() bool

StopNow()

TradeMode() TradeMode

SetOptions(options map[string]interface{}) error

Run() error

OnInit() error

OnTick() error

OnExit() error

}

Strategy interface

type StrategyBase ¶

type StrategyBase struct {

Exchanges []Exchange

Exchange Exchange

// contains filtered or unexported fields

}

StrategyBase Strategy base class

func (*StrategyBase) GetOptions ¶

func (s *StrategyBase) GetOptions() (optionMap map[string]*StrategyOption)

GetOptions Returns the options of strategy

func (*StrategyBase) IsStopped ¶

func (s *StrategyBase) IsStopped() bool

func (*StrategyBase) Name ¶

func (s *StrategyBase) Name() string

func (*StrategyBase) SetName ¶

func (s *StrategyBase) SetName(name string)

func (*StrategyBase) SetOptions ¶

func (s *StrategyBase) SetOptions(options map[string]interface{}) error

SetOptions Sets the options for the strategy

func (*StrategyBase) SetSelf ¶

func (s *StrategyBase) SetSelf(self Strategy) error

SetSelf 设置 self 对象

func (*StrategyBase) Setup ¶

func (s *StrategyBase) Setup(mode TradeMode, exchanges ...interface{}) error

Setup Setups the exchanges

func (*StrategyBase) StopNow ¶

func (s *StrategyBase) StopNow()

func (*StrategyBase) TradeMode ¶

func (s *StrategyBase) TradeMode() TradeMode

type StrategyOption ¶

type StrategyOption struct {

Name string `json:"name"`

Description string `json:"description"`

Type string `json:"type"`

Value interface{} `json:"value"`

DefaultValue interface{} `json:"default_value"`

}

StrategyOption 策略参数

type Trade ¶

type Trade struct {

ID string `json:"id"` // ID

Direction Direction `json:"type"` // 主动成交方向

Price float64 `json:"price"` // 价格

Amount float64 `json:"amount"` // 成交量(张),买卖双边成交量之和

Ts int64 `json:"ts"` // 订单成交时间 unix time (ms)

Symbol string `json:"omitempty"`

}

Trade 成交记录

type WebSocket ¶

type WebSocket interface {

SubscribeTrades(market Market, callback func(trades []Trade)) error

SubscribeLevel2Snapshots(market Market, callback func(ob *OrderBook)) error

//SubscribeBalances(market Market, callback func(balance *Balance)) error

SubscribeOrders(market Market, callback func(orders []Order)) error

SubscribePositions(market Market, callback func(positions []Position)) error

}

WebSocket 代表WS连接